Check out this video to learn more about the highly successful model David has infused into his planning process

In the realm of investment strategies, one of the more intriguing approaches is the endowment model, notably employed by large institutions like university endowments. This model, championed by figures like David Swensen of Yale University, offers unique insights for individual investors, especially those planning for retirement.

At its core, an endowment is a financial asset, like a fund, held by institutions such as universities. It’s made up of donations that are invested to generate income for the institution. The principal amount generally remains intact while the income supports various expenses.

The Yale endowment, under Swensen's management, became a hallmark of this approach. Yale’s strategy was not just successful but also revolutionary in how it diversified investments beyond the traditional stock and bond portfolio. This diversification aimed to achieve steady returns while minimizing risks.

Retirement planning can be akin to managing an endowment. In both cases, the goal is to create a sustainable income stream from a large pool of savings. The typical recommendation for endowment funds is to aim for a 5% annual distribution. This figure interestingly aligns with the retirement income strategies suggested by many financial planners.

However, a critical difference lies in the investment approach. Traditional retirement portfolios often focus heavily on stocks and bonds. In contrast, the endowment model advocates for a more diversified portfolio including alternative investments.

The endowment model’s success largely stems from its inclusion of alternative investments. These can range from private equity and hard assets like real estate to even more niche options like annuities. For instance, Yale’s portfolio in 2001 included a significant portion in hard assets, primarily real estate, alongside a smaller proportion in domestic and foreign equities.

This diversification strategy not only reduces reliance on the stock market but also potentially smoothens out returns, reducing volatility. The objective is to create a portfolio that can withstand market downturns better and provide more consistent returns over time.

Real estate, especially in sectors like student housing, is a prime example of an alternative investment that can offer stable returns. Properties near major universities, such as USC, Notre Dame, or Northwestern University, can provide a steady income stream, often with tax advantages.

Annuities are another diversifier in this model. While not directly linked to stock or bond markets, they can provide a steady income, adding another layer of stability to a retirement portfolio.

One of the key strengths of the endowment model is its use of non-correlated asset classes. Investments like real estate or annuities don’t necessarily move in tandem with the stock or bond markets. This non-correlation can significantly reduce the portfolio's overall risk.

For individual investors, adopting an endowment-like strategy means moving beyond the conventional wisdom of a stock-and-bond-dominated portfolio. It involves exploring and investing in a variety of asset classes. However, this approach requires careful planning and a thorough understanding of each investment type.

Given the complexity of this investment strategy, seeking professional advice is prudent. Financial advisors with experience in the endowment model can provide valuable insights and help tailor a portfolio that suits an individual’s retirement goals and risk tolerance.

The endowment model, inspired by the strategies of large institutions like Yale University, presents an innovative approach for individual investors, especially those in retirement planning.

Its focus on diversification across various asset classes aims to provide a balanced investment portfolio that can weather market volatility and generate sustainable income. While it may require stepping out of the traditional investment comfort zone, the potential for a more stable and robust retirement income is an enticing prospect for those willing to explore beyond stocks and bonds.

Check out this video to get some insight into David's personal story which lends to the purpose in his passion to help his clients achieve retirement success.

The world of retirement planning is deeply influenced by the personal experiences and histories of those who navigate it. One such journey, devoid of specific names but rich in lessons and insights, offers a valuable perspective on how early life experiences and family histories can shape professional philosophies in financial planning.

The story begins with a young individual, whose life was significantly impacted by their parents' divorce at the age of two. Raised by a single mother with two other children, this person found solace and guidance in the care of their grandparents. These formative years spent with grandparents in a small town provided foundational life lessons and values.

One grandparent, a dedicated employee at a major company like Sears Roebuck, which narrowly escaped bankruptcy, served as an emblem of resilience and adaptability. This grandparent's profession as a television repairman represented a now-obsolete trade, reflecting a bygone era of technological simplicity and hands-on skill.

The grandparent's investment in company stock, such as Sears, showcased the importance of financial involvement and awareness. This early exposure to stock investments and the significance of pension plans left a profound impact on the young individual, instilling a keen interest in financial planning and investment.

Despite modest means, the grandparent exemplified fiscal prudence and the virtue of saving, owning a home outright, and living within one's means. These characteristics were not just survival strategies but were also foundational principles that would later inform a career in financial planning.

A turning point in this narrative was the grandparent's diagnosis with dementia, leading to significant healthcare expenses that eventually depleted their savings. This transition to relying on Medicaid, a program necessitating minimal personal assets, highlighted the financial vulnerabilities faced in old age.

The family's subsequent struggle with a lien on their property due to Medicaid benefits underscored the complexities and challenges of elder care and its financial implications. This experience, occurring at the onset of the individual’s career in financial planning, was a catalyst for a deeper understanding of elder law and financial protection strategies.

These personal experiences with family financial challenges directly influenced the individual's approach to retirement planning. Observing first-hand the impact of medical expenses and the necessity of financial preparedness in later life, the individual adopted a philosophy emphasizing the protection of capital, its growth, and the generation of sustainable income from it.

This approach was further informed by the mindset of the "depression babies" generation, known for their skepticism towards banks and cautious approach to market investments. This background instilled a sensitivity towards clients who value security and stability in their financial planning.

This narrative, while not tied to a specific individual, illustrates how personal experiences can profoundly shape professional approaches in fields like financial planning. It's a poignant reminder that behind the technical aspects of financial advising are human stories, experiences, and histories that influence and guide the strategies and advice offered by professionals in this field.

In 1980, Ronald Reagan famously compared inflation to a violent mugger, a frightening armed robber, and a deadly hitman. During the tumultuous 1970s and early 1980s, inflation rates soared, averaging around 13.5%. This period of rampant inflation had a profound impact on the cost of goods, effectively doubling them within a decade.

While we might have experienced a reprieve from high inflation in recent years, it's crucial to recognize that it can rear its head once more. This article delves into the critical relationship between inflation and investing, highlighting the often-overlooked concept of the "perfect annuity" as a tool to combat the eroding effects of inflation in retirement.

Inflation is an ever-present economic phenomenon that erodes the purchasing power of money over time. When you invest, especially in long-term assets like stocks, the goal is to outpace inflation and preserve the value of your wealth.

Traditionally, many have seen investing in stocks as a hedge against inflation, with the assumption that equities can generate returns that outpace the rising cost of living. However, this assumption doesn't always hold true, as evidenced by events like the 2008 financial crisis, which wiped out substantial portions of many portfolios.

Investors often face the challenge of ensuring that their income and wealth can withstand the corrosive effects of inflation, especially in retirement. While the concept of the "perfect annuity" may sound like an ideal solution, it remains a relatively obscure strategy. In this article, we aim to shed light on this innovative approach to safeguarding retirement income while simultaneously battling inflation.

The "perfect annuity" is a financial strategy designed to provide guaranteed lifetime income while also offering protection against inflation. This concept is gaining traction among financial advisors and retirees for its potential to address two significant retirement concerns: longevity risk and inflation risk.

Consider a scenario where an individual has a retirement portfolio of approximately $1 million. By strategically allocating a portion of this portfolio to a perfect annuity, they can secure an annual income for life. Over a 20-year period, assuming a conservative annual growth rate, their income will almost double, providing a reliable hedge against inflation.

One of the significant advantages of the perfect annuity is its resemblance to a pension. In most cases, when you choose a joint life expectancy option, both spouses can enjoy the same income benefits. Moreover, if there's a remaining balance upon the passing of the annuitant and their spouse, it can be passed on to beneficiaries, such as children, providing a legacy that many traditional annuities do not offer.

Inflation is an ever-present financial adversary, and safeguarding your retirement income against its erosive effects is paramount. The "perfect annuity" represents a powerful and relatively undiscovered tool in this battle.

By combining guaranteed lifetime income with the potential for income growth that keeps pace with inflation, this strategy offers a compelling solution for retirees seeking financial security and peace of mind.

It's a strategy worth considering as you plan for your retirement years and aim to ensure that your income not only lasts a lifetime but also remains resilient in the face of inflation's challenges.

As individuals approach retirement, it becomes increasingly vital to engage with financial professionals who can provide guidance on creating a secure financial future. This article focuses on the importance of comprehending your investment portfolio and the benefits of working with knowledgeable advisors in this regard.

Surprisingly, research shows that only a small fraction of investors truly understand the composition of their investment funds. This lack of knowledge can pose significant challenges, as it limits one's ability to make informed financial decisions, especially when planning for retirement.

A holistic approach to retirement planning involves gaining a deep understanding of your investment portfolio. Advisors who take this approach spend considerable time dissecting your portfolio, explaining its nuances, and ensuring that you comprehend its components. Whether you are well-versed in financial matters or not, this personalized education is crucial.

One fundamental aspect of comprehensive retirement planning is the evaluation of your investment portfolio's resilience. Advisors often perform what is known as a "portfolio stress test." This in-depth analysis assesses the allocation between stocks and bonds and evaluates the overall risk profile. Understanding these factors is essential, particularly when considering the potential impact of economic downturns.

It's important to recognize that investments extend beyond traditional stocks and bonds. Diversification into alternative assets can help reduce portfolio risk. Over-reliance on the performance of stock and bond markets can be risky, as these markets can be volatile. Incorporating a range of assets outside the mainstream can provide a more stable financial foundation.

To illustrate the importance of portfolio understanding, let's consider a hypothetical case. Susan, a retiree with a substantial portfolio, became concerned about her investments' performance. Upon a detailed examination, it was discovered that her bond holdings were suffering due to rising interest rates. This case highlights the necessity of monitoring and adjusting portfolios to adapt to changing market conditions.

In summary, comprehensive retirement planning involves gaining a clear understanding of your investment portfolio. This knowledge empowers you to make well-informed financial decisions, ensuring a more secure retirement.

By undergoing portfolio stress testing and diversifying investments across various asset classes, individuals can enhance the resilience of their financial portfolios. This approach remains critical in today's uncertain financial landscape, providing a pathway to a financially secure retirement.

Watch this informative and interactive video to learn more about our services!

In the complex world of finance, selecting a qualified financial advisor is crucial for ensuring effective management of your financial assets. Financial industries, recognizing the need for establishing benchmarks of excellence, have developed various accreditation programs.

These programs serve as a beacon, guiding individuals in choosing competent financial advisors equipped with the necessary skills and knowledge. Below is an overview of some prominent designations you should consider when selecting a financial advisor.

The Certified Financial Planner (CFP) is among the most sought-after designations in financial planning. To earn the CFP title, candidates must excel in four core areas: Education, Examination, Experience, and Ethics.

This comprehensive approach ensures that CFP professionals are well-equipped to offer sound financial planning advice. They undergo rigorous academic training, covering a wide range of topics including retirement planning, estate planning, risk management, and tax planning.

The examination phase is exhaustive, testing their practical application skills and theoretical knowledge. Furthermore, they must accumulate substantial real-world experience before they can be certified. Finally, adherence to high ethical standards is mandatory, ensuring that a CFP acts in the best interest of their clients.

The Chartered Financial Consultant (ChFC) designation is similar to the CFP in many respects, particularly in the depth and breadth of financial knowledge required. However, one key difference is the absence of a comprehensive board examination in the ChFC certification process.

ChFC professionals specialize in all aspects of financial planning, including insurance, income taxation, retirement planning, investments, and estate planning. This designation is often pursued by professionals who wish to deepen their understanding of financial planning without undergoing the CFP’s rigorous examination process.

The Chartered Life Underwriter (CLU) is the premier designation for professionals specializing in life insurance and estate planning. Regarded as the most respected insurance designation, the CLU equips professionals with in-depth knowledge of various life insurance products and a comprehensive understanding of the legal, financial, and tax aspects of estate planning.

This designation is particularly valuable for individuals seeking expert guidance in life insurance and estate management.

A Certified Public Accountant (CPA) is a professional who has excelled in the realm of accounting. To attain the CPA designation, one must complete the required college courses, earn a bachelor’s degree, and pass a rigorous 19-hour examination spread over two days. CPAs specialize in various aspects of financial management, including taxes, auditing, and bookkeeping. Their expertise is particularly vital in navigating complex tax laws and ensuring accurate financial reporting and auditing.

The Chartered Financial Analyst (CFA) designation is highly coveted in the field of investment management. To become a CFA, candidates must undergo a demanding course of study and pass a series of challenging exams.

The focus of the CFA program is investment analysis and portfolio management. CFAs are renowned for their expertise in financial analysis, valuation, asset management, and the application of ethical and professional standards in investment management.

The financial industry is constantly evolving, leading to the emergence of new designations. While these new credentials may offer specialized knowledge in certain areas, it's important to note that not all are as rigorously tested as the CFP and CPA designations.

As the financial landscape becomes increasingly complex, these designations play a pivotal role in defining the standards of professionalism and competence.

Choosing a financial advisor with the right designation is a crucial step in ensuring that your financial needs are adequately addressed. Each designation signifies a different area of expertise and a different approach to financial management.

It's essential to select a professional who not only holds a relevant designation but also understands your unique financial situation and goals. Look for advisors who are committed to aligning their expertise with your specific needs.

When selecting a financial advisor, the array of designations can be overwhelming. However, understanding these key designations – CFP, ChFC, CLU, CPA, and CFA – can significantly aid in making an informed choice. Remember, the right financial advisor is not just about credentials; it's also about finding someone who can tailor their expertise to your individual needs.

Always inquire about their experience, their approach to financial planning, and how they intend to meet your specific requirements. With the right advisor, you can navigate the complexities of financial planning with confidence and clarity

.

The Little Red Book of Retirement Chapter 1

Retirement planning is a topic of paramount importance, especially for high net worth individuals. The first chapter of "The Little Red Book of Retirement" offers critical insights into the unique retirement planning needs of these individuals. This chapter lays the foundation for understanding how high net worth clients can strategically manage their wealth for a secure and fulfilling retirement.

High net worth individuals, typically defined as those with a net worth exceeding $1 million, face unique challenges and opportunities in retirement planning. This chapter emphasizes that their retirement strategy needs to go beyond basic savings and investment plans. It should encompass a comprehensive approach that considers various financial and lifestyle aspects.

The first chapter of the book underscores the importance of partnering with specialized financial advisors. These professionals bring expertise in managing complex financial portfolios and can provide invaluable guidance on investment strategies, tax planning, estate management, and retirement income planning.

Chapter 1 of "The Little Red Book of Retirement" provides a comprehensive overview of the critical aspects of retirement planning for high net worth individuals. It emphasizes the need for a tailored approach that addresses the specific financial and lifestyle goals of the affluent. By understanding these key principles and working with experienced financial advisors, high net worth individuals can effectively navigate the challenges of retirement planning, ensuring financial stability and a fulfilling post-career life.

Welcome, readers, to this insightful article on revolutionizing retirement planning. In today's discussion, we will explore key concepts from a recent book focusing on retirement preparation. Over a series of articles, we will delve into the core principles that aim to reshape how we approach retirement.

In 1995, one individual entered the financial advisory business with dreams of making a difference in the lives of retirees. Little did they know that a deeply personal experience would significantly impact their outlook on financial planning. This poignant story demonstrates the importance of comprehensive retirement planning.

Many individuals may find themselves lacking the necessary knowledge and resources to navigate retirement planning effectively. Traditional financial advisors often concentrate on asset allocation, presenting visually appealing charts that may not provide the best protection against capital loss during retirement.

During the 2008 financial crisis, many retirees discovered the limitations of traditional diversification strategies. Despite being told that a balanced portfolio of stocks and bonds was a conservative approach, they experienced substantial losses. These events highlighted the need for more robust retirement planning.

To address the shortcomings in retirement planning, a more comprehensive and integrated strategy is essential. This approach goes beyond traditional asset allocation and introduces the concept of a "retirement income distribution plan." This plan is designed to stress-test assets, minimize fees, and provide a customized roadmap for each individual's unique financial situation.

Diversification should extend beyond asset classes and encompass various investment strategies. For instance, real estate investments can provide stability since they often perform independently of the stock market. By incorporating such non-correlated assets into your portfolio, you can reduce vulnerability during market downturns.

Diversification alone may not be enough to protect your portfolio during market volatility. Implementing risk management strategies is crucial. One such strategy is a "stop loss" mechanism, which caps losses at a predetermined percentage. This approach acts as a safeguard against significant portfolio declines during turbulent market conditions.

In this article, we have explored innovative concepts in retirement planning that aim to improve financial security during one's retirement years. The emphasis has been on comprehensive, integrated planning that surpasses traditional asset allocation.

The goal is to protect against risk and enhance returns for a more secure financial future. Stay tuned for the upcoming articles in this series, where we will delve deeper into these innovative strategies.

https://www.youtube.com/watch?v=8JUi3srJWs4&t=3s

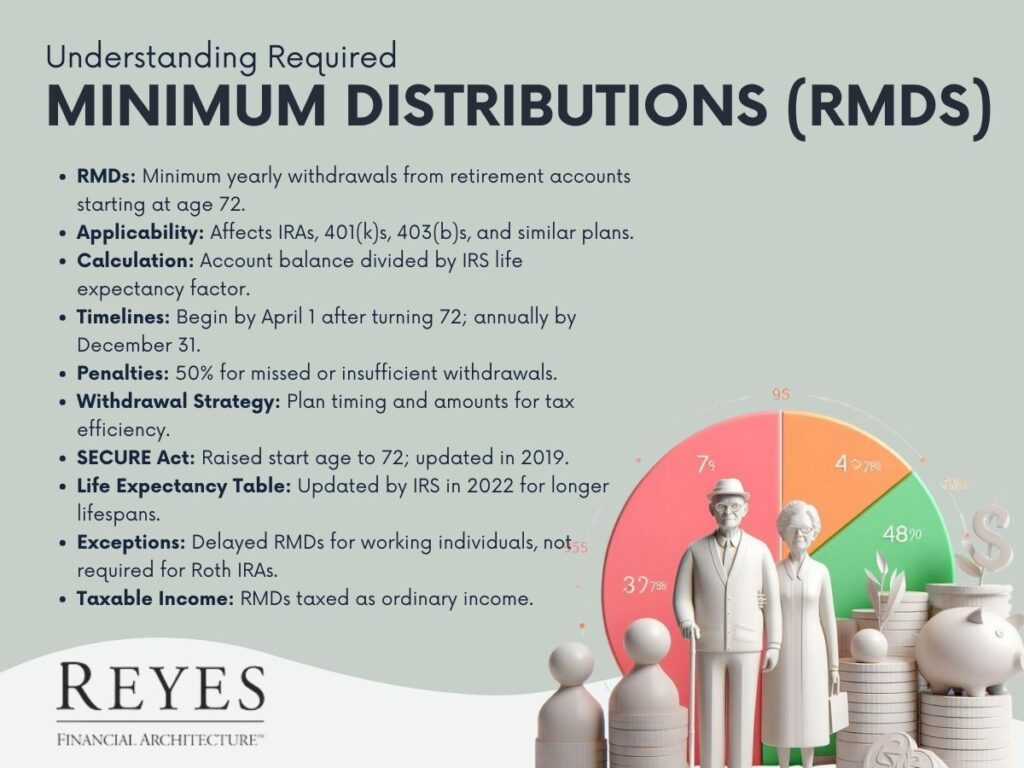

Click on the link to watch the attached video to learn more about: What are RMD's and How are they Determined?

When it comes to retirement planning, understanding Required Minimum Distributions (RMDs) is crucial. Essentially, RMDs are the minimum amounts that a retirement plan account owner must withdraw annually, starting with the year they reach 70.5 years of age or, if later, the year they retire.

RMDs apply to tax-deferred retirement accounts. These accounts include IRAs, 401(k)s, 403(b)s, and other defined contribution plans. The rationale behind RMDs is straightforward: since contributions to these accounts are often tax-deductible, and the growth in the accounts is tax-deferred, RMDs ensure that this untaxed money is eventually subject to taxation.

The amount of an RMD is determined by dividing the account balance as of December 31 of the preceding year by a life expectancy factor set by the IRS. For example, at age 70, the life expectancy factor is 27.4 years. This means if a retiree has a retirement account balance of $100,000 at the end of the year, their RMD would be approximately $3,649 (100,000 divided by 27.4).

Understanding and planning for RMDs is a critical component of retirement planning. Failure to take an RMD, or withdrawing too little, can result in significant penalties – typically 50% of the amount that should have been withdrawn. Hence, it's essential for retirees to:

As of my last update in April 2023, there have been changes to the rules governing RMDs:

RMDs are taxable as ordinary income in the year they are withdrawn. Tax planning strategies, such as spreading out large expenses or deductions over several years, can help manage the tax burden associated with RMDs.

Required Minimum Distributions are a key aspect of retirement planning, especially for those with tax-deferred retirement accounts. Understanding how they are calculated, the timelines involved, and the strategies for managing them can have a significant impact on retirement income and taxation. With careful planning and, if necessary, professional advice, retirees can navigate RMDs effectively to optimize their retirement finances.

For a more personalized approach to RMDs and retirement strategy, consulting with a financial advisor is recommended. They can provide tailored advice and calculations based on individual circumstances, ensuring a comfortable and financially secure retirement.

Click on the link to watch our interactive video to quickly and simply understand: How to Strategize for your Social Security Benefits.

Social Security serves as a foundational element in many retirement plans, and understanding how to strategize for maximum benefits is crucial. With increasing life expectancies, retirement can last between 20 to 30 years, making Social Security planning more critical than ever. This blog explores the strategies for optimizing Social Security benefits, helping ensure a financially secure retirement.

The Social Security system in the United States is designed to provide financial support to individuals in their retirement years. The amount of benefit one receives is based on their 35 highest-earning years of work. The full retirement age (FRA) – the age at which one is eligible for full benefits – varies from 66 to 67, depending on the birth year.

The age at which you start claiming Social Security benefits significantly impacts the amount received. Claiming benefits at the earliest age of 62 results in a reduction of at least 25% compared to waiting until the full retirement age. Conversely, delaying benefits past the FRA up to age 70 leads to an increase in benefits, with a maximum increase of 32% at age 70.

For example, if the retirement income at age 66 is $2,000 per month, retiring at this age versus waiting until age 70 can mean a difference of over $200,000 over a lifetime. This stark difference underscores the importance of timing in Social Security planning.

Couples have additional strategies available. Spouses can claim benefits based on their work record or receive up to 50% of their spouse’s benefit at full retirement age, whichever is higher. Coordinating the timing of benefit claims can maximize total household Social Security income. For example, the lower-earning spouse might start benefits earlier, while the higher-earning spouse delays benefits to increase the survivor benefit.

Working while receiving Social Security benefits before reaching the full retirement age can temporarily reduce your benefits. Understanding these rules is vital for those planning to work part-time in retirement. After reaching the full retirement age, however, earnings do not affect Social Security benefits.

Up to 85% of Social Security benefits can be taxable, depending on your total income. Planning for tax implications is essential. Strategies like Roth IRA conversions or timing the withdrawal of retirement accounts can impact the taxation of Social Security benefits and overall retirement income.

Repositioning assets to reduce taxable income can lead to more tax-efficient retirement income. This might involve shifting from taxable accounts to Roth IRAs or employing tax-loss harvesting strategies. This repositioning can influence the taxation of Social Security benefits, potentially leading to lower overall tax liabilities.

With over 500 possible combinations of factors affecting benefits, consulting a financial advisor who specializes in Social Security planning is highly recommended. An advisor can offer customized strategies based on individual circumstances and help navigate the complex rules of the Social Security system.

Social Security planning should be a personalized process, reflecting individual work histories, health status, family circumstances, and retirement goals. The decision on when to claim benefits is a pivotal one, with long-lasting financial implications.

Understanding the nuances of the Social Security system and employing strategic planning can make a significant difference in retirement income, ensuring a more secure and comfortable retirement phase.

As retirements grow longer, the importance of maximizing Social Security benefits cannot be overstated. It's not just about when to start claiming benefits but how to integrate them with other retirement income sources, tax planning, and spousal benefits. Informed decisions and strategic planning in this arena are invaluable for achieving a financially stable and fulfilling retirement.