Learn How to Invest in Student Housing

Special guest: Brian Nelson from NB Private Capital

Investing in real estate is a time-honored strategy for building wealth, and within the vast realm of real estate investments, student housing emerges as a unique and potentially lucrative niche. This article delves into the reasons why student housing can be an attractive investment, the differences from other real estate investments, and the strategies investors use to capitalize on this sector.

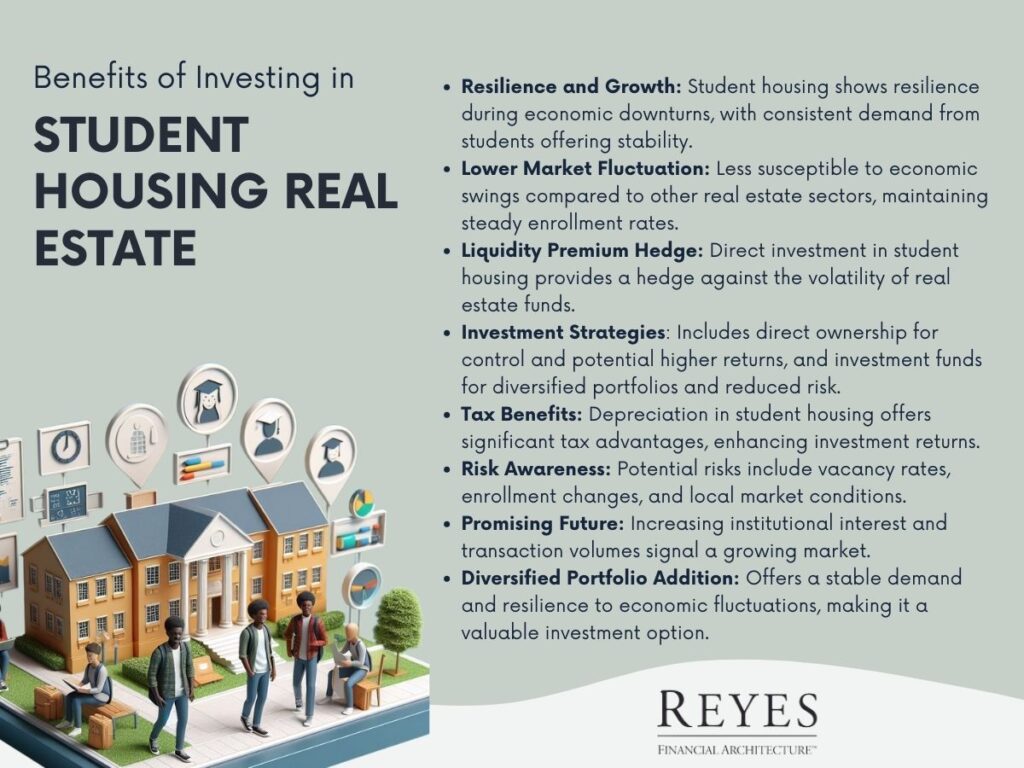

Student housing refers to properties specifically designed or utilized to accommodate college or university students. Unlike traditional residential real estate, these properties often have unique characteristics tailored to the needs and lifestyles of students. This market segment has gained attention for its resilience and growth potential, especially in prime locations near educational institutions.

One of the most compelling aspects of investing in student housing is its resilience to economic downturns. Historical data suggests that during the 2008-2010 financial crisis, while most real estate sectors suffered significant devaluation, student housing was one of the few categories where values increased. This resilience can be attributed to the consistent demand for housing from students, which remains relatively stable irrespective of economic conditions. Additionally, the sector has witnessed consistent growth, with annual transaction volumes increasing significantly over the years.

The primary distinction between student housing and other types of real estate investments lies in its lower cyclical nature and reduced susceptibility to market fluctuations. Unlike commercial or conventional residential real estate, the demand for student housing is less influenced by economic swings, as enrollment rates tend to remain steady or even increase during recessions.

In the world of real estate investment, owning hard assets like student housing offers a hedge against the liquidity premium associated with real estate funds. In stark contrast to real estate mutual funds, which can experience significant value drops in volatile markets, physical real estate assets usually do not depreciate as drastically. This stability is particularly evident in student housing, where the inherent demand provides an additional layer of security.

Investors approach student housing through two primary strategies: direct ownership and investment funds. Direct ownership involves purchasing individual properties, often leveraging strategies such as 1031 exchanges to optimize tax benefits. This approach suits investors seeking direct control and the potential for higher individual property returns.

Alternatively, investment funds in student housing allow investors to pool their resources and invest in a diversified portfolio of properties. These funds typically own multiple properties across different locations, offering investors a share in a broader range of assets. This diversification reduces the risk associated with individual property performance and provides a more stable income stream.

A significant advantage of investing in student housing, particularly in the U.S., is the ability to leverage depreciation for tax benefits. Commercial real estate, including student housing, offers opportunities for investors to shelter income through depreciation, thereby enhancing the overall return on investment.

While student housing offers many benefits, investors must be aware of potential risks. These include the possibility of vacancy rates affecting income, changes in university enrollment patterns, and local market conditions that might impact property values. However, careful property selection, especially in markets with strong demand and limited supply, can mitigate these risks.

The future of student housing investments looks promising, with increasing institutional interest and growing transaction volumes in the sector. As more investors recognize the unique benefits and potential of this market, the demand for quality student housing is expected to rise, especially in fast-growing educational markets.

In summary, student housing presents a compelling investment opportunity, offering resilience to economic fluctuations, potential tax benefits, and stable demand. Whether through direct property ownership or participation in investment funds, this sector can be a valuable addition to a diversified investment portfolio. However, as with any investment, it is essential to understand the risks and conduct thorough market research to maximize returns.