Watch this informative and interactive video to learn more about our services!

In the complex world of finance, selecting a qualified financial advisor is crucial for ensuring effective management of your financial assets. Financial industries, recognizing the need for establishing benchmarks of excellence, have developed various accreditation programs.

These programs serve as a beacon, guiding individuals in choosing competent financial advisors equipped with the necessary skills and knowledge. Below is an overview of some prominent designations you should consider when selecting a financial advisor.

1. Certified Financial Planner (CFP)

The Certified Financial Planner (CFP) is among the most sought-after designations in financial planning. To earn the CFP title, candidates must excel in four core areas: Education, Examination, Experience, and Ethics.

This comprehensive approach ensures that CFP professionals are well-equipped to offer sound financial planning advice. They undergo rigorous academic training, covering a wide range of topics including retirement planning, estate planning, risk management, and tax planning.

The examination phase is exhaustive, testing their practical application skills and theoretical knowledge. Furthermore, they must accumulate substantial real-world experience before they can be certified. Finally, adherence to high ethical standards is mandatory, ensuring that a CFP acts in the best interest of their clients.

2. Chartered Financial Consultant (ChFC)

The Chartered Financial Consultant (ChFC) designation is similar to the CFP in many respects, particularly in the depth and breadth of financial knowledge required. However, one key difference is the absence of a comprehensive board examination in the ChFC certification process.

ChFC professionals specialize in all aspects of financial planning, including insurance, income taxation, retirement planning, investments, and estate planning. This designation is often pursued by professionals who wish to deepen their understanding of financial planning without undergoing the CFP’s rigorous examination process.

3. Chartered Life Underwriter (CLU)

The Chartered Life Underwriter (CLU) is the premier designation for professionals specializing in life insurance and estate planning. Regarded as the most respected insurance designation, the CLU equips professionals with in-depth knowledge of various life insurance products and a comprehensive understanding of the legal, financial, and tax aspects of estate planning.

This designation is particularly valuable for individuals seeking expert guidance in life insurance and estate management.

4. Certified Public Accountant (CPA)

A Certified Public Accountant (CPA) is a professional who has excelled in the realm of accounting. To attain the CPA designation, one must complete the required college courses, earn a bachelor’s degree, and pass a rigorous 19-hour examination spread over two days. CPAs specialize in various aspects of financial management, including taxes, auditing, and bookkeeping. Their expertise is particularly vital in navigating complex tax laws and ensuring accurate financial reporting and auditing.

5. Chartered Financial Analyst (CFA)

The Chartered Financial Analyst (CFA) designation is highly coveted in the field of investment management. To become a CFA, candidates must undergo a demanding course of study and pass a series of challenging exams.

The focus of the CFA program is investment analysis and portfolio management. CFAs are renowned for their expertise in financial analysis, valuation, asset management, and the application of ethical and professional standards in investment management.

New and Emerging Designations

The financial industry is constantly evolving, leading to the emergence of new designations. While these new credentials may offer specialized knowledge in certain areas, it's important to note that not all are as rigorously tested as the CFP and CPA designations.

As the financial landscape becomes increasingly complex, these designations play a pivotal role in defining the standards of professionalism and competence.

The Importance of Choosing the Right Advisor

Choosing a financial advisor with the right designation is a crucial step in ensuring that your financial needs are adequately addressed. Each designation signifies a different area of expertise and a different approach to financial management.

It's essential to select a professional who not only holds a relevant designation but also understands your unique financial situation and goals. Look for advisors who are committed to aligning their expertise with your specific needs.

Conclusion

When selecting a financial advisor, the array of designations can be overwhelming. However, understanding these key designations – CFP, ChFC, CLU, CPA, and CFA – can significantly aid in making an informed choice. Remember, the right financial advisor is not just about credentials; it's also about finding someone who can tailor their expertise to your individual needs.

Always inquire about their experience, their approach to financial planning, and how they intend to meet your specific requirements. With the right advisor, you can navigate the complexities of financial planning with confidence and clarity

.

The Little Red Book of Retirement Chapter 1

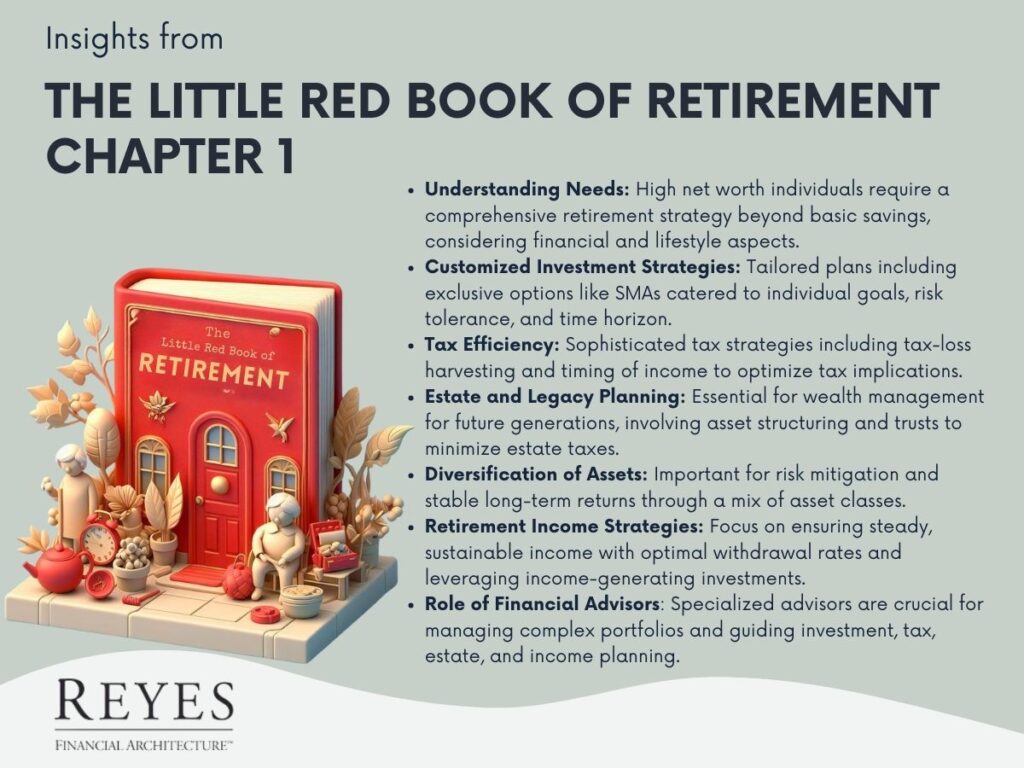

Retirement planning is a topic of paramount importance, especially for high net worth individuals. The first chapter of "The Little Red Book of Retirement" offers critical insights into the unique retirement planning needs of these individuals. This chapter lays the foundation for understanding how high net worth clients can strategically manage their wealth for a secure and fulfilling retirement.

Understanding High Net Worth Retirement Needs

High net worth individuals, typically defined as those with a net worth exceeding $1 million, face unique challenges and opportunities in retirement planning. This chapter emphasizes that their retirement strategy needs to go beyond basic savings and investment plans. It should encompass a comprehensive approach that considers various financial and lifestyle aspects.

Key Components of High Net Worth Retirement Planning

Customized Investment Strategies: High net worth individuals benefit from investment plans tailored to their specific financial goals, risk tolerance, and time horizon. These customized strategies often include access to exclusive investment options like separately managed accounts (SMAs).

Tax Efficiency: Effective retirement planning for the affluent involves sophisticated tax strategies. This can include tax-loss harvesting, timing of income, and considering the tax implications of various retirement accounts.

Estate and Legacy Planning: This chapter highlights the importance of estate planning in securing and managing wealth for future generations. This involves structuring assets to reduce estate taxes and setting up trusts or other legal structures.

Diversification of Assets: Diversifying investment portfolios to include a mix of asset classes is crucial for high net worth individuals. This approach helps in mitigating risks and achieving more stable long-term returns.

Retirement Income Strategies: The chapter delves into strategies for ensuring a steady and sustainable income during retirement. This includes determining the optimal withdrawal rate from retirement accounts and potentially leveraging annuities or other income-generating investments.

The Role of Financial Advisors in High Net Worth Retirement Planning

The first chapter of the book underscores the importance of partnering with specialized financial advisors. These professionals bring expertise in managing complex financial portfolios and can provide invaluable guidance on investment strategies, tax planning, estate management, and retirement income planning.

Conclusion

Chapter 1 of "The Little Red Book of Retirement" provides a comprehensive overview of the critical aspects of retirement planning for high net worth individuals. It emphasizes the need for a tailored approach that addresses the specific financial and lifestyle goals of the affluent. By understanding these key principles and working with experienced financial advisors, high net worth individuals can effectively navigate the challenges of retirement planning, ensuring financial stability and a fulfilling post-career life.

Welcome, readers, to this insightful article on revolutionizing retirement planning. In today's discussion, we will explore key concepts from a recent book focusing on retirement preparation. Over a series of articles, we will delve into the core principles that aim to reshape how we approach retirement.

A Personal Insight

In 1995, one individual entered the financial advisory business with dreams of making a difference in the lives of retirees. Little did they know that a deeply personal experience would significantly impact their outlook on financial planning. This poignant story demonstrates the importance of comprehensive retirement planning.

The Shortcomings in Retirement Planning

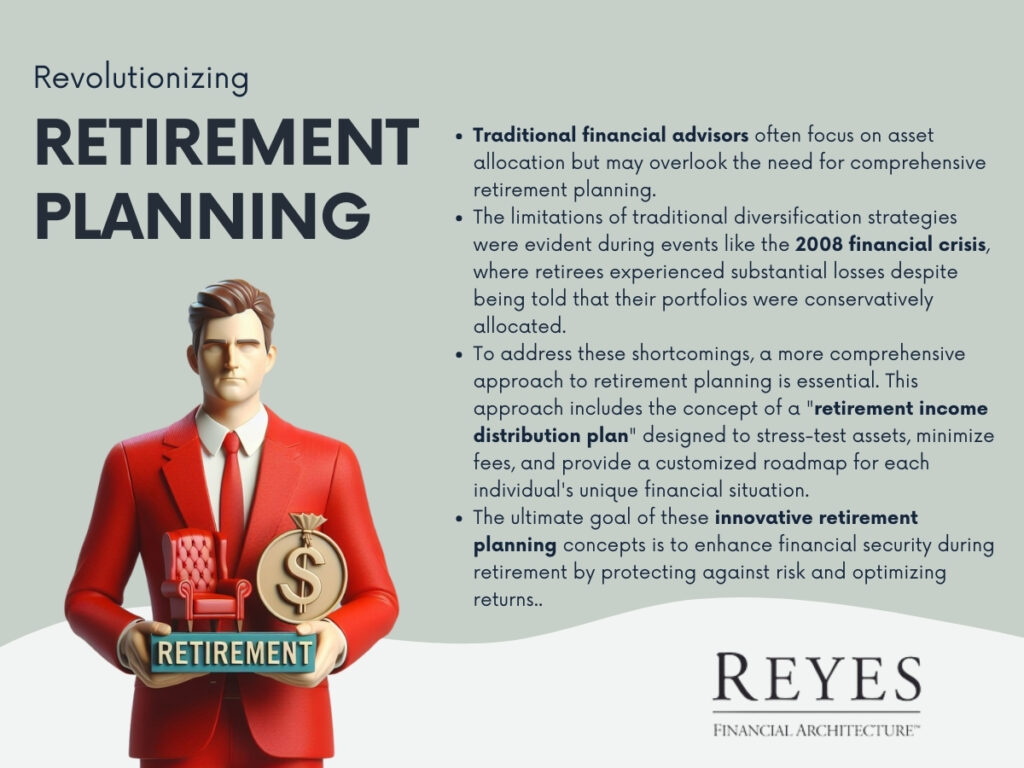

Many individuals may find themselves lacking the necessary knowledge and resources to navigate retirement planning effectively. Traditional financial advisors often concentrate on asset allocation, presenting visually appealing charts that may not provide the best protection against capital loss during retirement.

Diversification Alone Falls Short

During the 2008 financial crisis, many retirees discovered the limitations of traditional diversification strategies. Despite being told that a balanced portfolio of stocks and bonds was a conservative approach, they experienced substantial losses. These events highlighted the need for more robust retirement planning.

The Call for a Comprehensive Approach

To address the shortcomings in retirement planning, a more comprehensive and integrated strategy is essential. This approach goes beyond traditional asset allocation and introduces the concept of a "retirement income distribution plan." This plan is designed to stress-test assets, minimize fees, and provide a customized roadmap for each individual's unique financial situation.

Diversify Across Strategies

Diversification should extend beyond asset classes and encompass various investment strategies. For instance, real estate investments can provide stability since they often perform independently of the stock market. By incorporating such non-correlated assets into your portfolio, you can reduce vulnerability during market downturns.

Implementing Risk Management

Diversification alone may not be enough to protect your portfolio during market volatility. Implementing risk management strategies is crucial. One such strategy is a "stop loss" mechanism, which caps losses at a predetermined percentage. This approach acts as a safeguard against significant portfolio declines during turbulent market conditions.

Conclusion

In this article, we have explored innovative concepts in retirement planning that aim to improve financial security during one's retirement years. The emphasis has been on comprehensive, integrated planning that surpasses traditional asset allocation.

The goal is to protect against risk and enhance returns for a more secure financial future. Stay tuned for the upcoming articles in this series, where we will delve deeper into these innovative strategies.

https://youtu.be/LlSuazb60RI?feature=shared

Click on the link to watch our interactive video to quickly and simply understand: How to Strategize for your Social Security Benefits.

Social Security serves as a foundational element in many retirement plans, and understanding how to strategize for maximum benefits is crucial. With increasing life expectancies, retirement can last between 20 to 30 years, making Social Security planning more critical than ever. This blog explores the strategies for optimizing Social Security benefits, helping ensure a financially secure retirement.

1. Understanding the Basics of Social Security

The Social Security system in the United States is designed to provide financial support to individuals in their retirement years. The amount of benefit one receives is based on their 35 highest-earning years of work. The full retirement age (FRA) – the age at which one is eligible for full benefits – varies from 66 to 67, depending on the birth year.

2. Deciding When to Claim Benefits

The age at which you start claiming Social Security benefits significantly impacts the amount received. Claiming benefits at the earliest age of 62 results in a reduction of at least 25% compared to waiting until the full retirement age. Conversely, delaying benefits past the FRA up to age 70 leads to an increase in benefits, with a maximum increase of 32% at age 70.

Case Study:

For example, if the retirement income at age 66 is $2,000 per month, retiring at this age versus waiting until age 70 can mean a difference of over $200,000 over a lifetime. This stark difference underscores the importance of timing in Social Security planning.

3. Coordinating Benefits with Your Spouse

Couples have additional strategies available. Spouses can claim benefits based on their work record or receive up to 50% of their spouse’s benefit at full retirement age, whichever is higher. Coordinating the timing of benefit claims can maximize total household Social Security income. For example, the lower-earning spouse might start benefits earlier, while the higher-earning spouse delays benefits to increase the survivor benefit.

4. Consider Work and Earnings

Working while receiving Social Security benefits before reaching the full retirement age can temporarily reduce your benefits. Understanding these rules is vital for those planning to work part-time in retirement. After reaching the full retirement age, however, earnings do not affect Social Security benefits.

5. Taxation of Social Security Benefits

Up to 85% of Social Security benefits can be taxable, depending on your total income. Planning for tax implications is essential. Strategies like Roth IRA conversions or timing the withdrawal of retirement accounts can impact the taxation of Social Security benefits and overall retirement income.

6. Asset Repositioning for Tax Efficiency

Repositioning assets to reduce taxable income can lead to more tax-efficient retirement income. This might involve shifting from taxable accounts to Roth IRAs or employing tax-loss harvesting strategies. This repositioning can influence the taxation of Social Security benefits, potentially leading to lower overall tax liabilities.

7. Seeking Professional Advice

With over 500 possible combinations of factors affecting benefits, consulting a financial advisor who specializes in Social Security planning is highly recommended. An advisor can offer customized strategies based on individual circumstances and help navigate the complex rules of the Social Security system.

Conclusion: A Tailored Approach for Optimal Benefits

Social Security planning should be a personalized process, reflecting individual work histories, health status, family circumstances, and retirement goals. The decision on when to claim benefits is a pivotal one, with long-lasting financial implications.

Understanding the nuances of the Social Security system and employing strategic planning can make a significant difference in retirement income, ensuring a more secure and comfortable retirement phase.

As retirements grow longer, the importance of maximizing Social Security benefits cannot be overstated. It's not just about when to start claiming benefits but how to integrate them with other retirement income sources, tax planning, and spousal benefits. Informed decisions and strategic planning in this arena are invaluable for achieving a financially stable and fulfilling retirement.

Evensky, Carson and others offer strong reactions to the legendary investor’s prediction about demise of RIAs

ThinkAdvisor’s Nov. 21 interview with Ken Fisher in which the renowned money manager forecast the demise of the RIA world in 10 years ignited a fire under advisors.

Fisher predicted that, if the fiduciary features of Dodd-Frank are implemented, BDs would absorb and, in essence, exterminate RIAs. He cited the size and wealth of BDs, as well as the Financial Industry Regulatory Authority’s superior lobbying power on the fiduciary issue.

Though his forecast blared a loud Reveille, RIAs have no intention to get ready for Taps, advisors like Harold Evensky told ThinkAdvisor, echoed by several commenters on the article — though others, like Ron Carson, say the famed investor has a valid point.

“Fisher is wrong once again," Joe Gordon said in a comment to the story, "as the RIA industry, with a small budget and little unity in politics and lobbying, can come together [as] David fighting Goliath. What is the true relevance of a BD? Signing leases and buying copiers? … The CFP Board of Standards, et al, needs to [toughen up] rather than tolerate fewer fee renewals if they stand up to Wall Street.”

In an interview with ThinkAdvisor, Harold Evensky, president-principal of the Coral Gables, Fla.-based fee-only firm Evensky & Katz, and a member of the Committee for the Fiduciary Standard, which advocates for an undiluted fiduciary standard for FAs, says: “It’s not going to be as disastrous as Ken suggests. I certainly don’t think the RIAs in general will go out of business.”

And in San Diego, Calif., David Reyes, RIA and founder of Reyes Financial Architecture, told ThinkAdvisor: “I disagree with Ken 150%. He’s obviously coming from the BD point of view. The BD community has no incentive to have the fiduciary standard. The Morgan Stanleys and Merrill Lynches of the world have fought it because with the suitability standard, conflicts of interest don’t have to be disclosed, and they can charge higher fees for their own products, which are highly profitable. Why would they want to be a fiduciary? It doesn’t make sense.”

Merrill Lynch, Morgan Stanley, Wells Fargo, Raymond James and Commonwealth Financial Network declined to comment for this story.

Some advisors think Fisher’s alarm is pitch-perfect.

“Ken has nailed down a very important issue for the industry,” says Clark Blackman, RIA, president and CEO of Alpha Wealth Strategies in Kingwood, Texas. "I agree that [RIAs' demise] certainly can happen and may happen — but it doesn’t have to happen."

RIAs’ savior may be the hybrid model, one that Fisher assails for misrepresenting many BD advisors as fee-only advisors.

In the meantime, says Carol Rogers, president of Rogers & Co. in St. Louis, “the fear of RIAs being gone may push them more into being hybrids in conjunction with some of the BDs. This is becoming a huge, huge trend with independent advisors.”

This year Rogers finalized a strategic alliance with V Wealth Management, a hybrid in Overland, Kansas. Both firms are affiliated with LPL Financial.

“I don’t want to be an independent RIA because of the complex compliance demand," Rogers says. "I want that double security of having a broker-dealer behind me as well as an RIA.”

But Evensky worries that, with the hybrid model, “Where does the buck stop? The risk is what we’ve referred to for decades as ‘hat-switching.’ The investor goes into an RIA; and then they pass them off to the brokerage, who does the implementation. If that’s allowed, it becomes a sham. If someone meets with an advisor and a level of trust is established, you can’t change and say, ‘OK, you could trust me when I was a fiduciary, when we started; but now that we’re going to implement, all bets are off. You’re on your own. Caveat emptor.’”

Blackman strongly concurs. With a hybrid, “if the client ends up being sold a product, it has to be done as a fiduciary, not as a salesman on a suitability standard, he said. "But the fiduciary standard is an extremely difficult one to meet when you’re selling a product.”

Most of the advisors agree, however, that smaller RIAs will soon vanish.

“Ken is absolutely right: the little RIAs aren’t going to survive,” Rogers says. “They’ll either join a hybrid firm or go back to a BD because the complexity is just too overwhelming.”

Ron Carson, founder of Carson Wealth Management Group, a hybrid, and Carson Institutional Alliance, in Omaha, Nebraska, disagrees with Fisher’s charge that RIAs are “naïve” to think they aren’t in jeopardy. “The RIA world is very sophisticated and getting more so all the time because the smaller ones are having to merge, consolidate or go out of business,” he says.

Fisher maintains that BDs want FINRA to take over regulating the RIAs. Indeed, FINRA has been lobbying aggressively toward this end.

If they win, what follows seems to be inevitable.

“As Ken Fisher observed, Wall Street does not like to see its market share decline," Ron Rhoades, assistant professor-chairman of Alfred State Financial Planning Program in Rochester, N.Y., and a former chairman of the National Association of Personal Financial Advisors (NAPFA), notes in an article comment. "Hence, FINRA will likely (after gaining oversight of RIAs) issue a host of new regulations, making it difficult for any RIA-only firm to survive.”

Blackman is in accord with that view, and then some. “If FINRA gets its way to be overseer of all advisors, then the fee-only RIA model is in serious trouble," he says. "FINRA would like to reinvent the wheel and have everybody be like them, even though they’re the ones that crept into a different business model and are now trying to usurp it. BDs have moved into the advisory space but without giving up the model of selling product – and the public can’t tell the difference.”

Blackman continues. “It’s getting to the point where it’s now or never. FINRA isn’t backing off. Remember, they’re still the National Association of Securities Dealers (NASD) — because even if they change their name, as they’ve done, it doesn’t change who they are.

“The broker-dealer world is losing clients and big advisors in droves,” Blackman goes on. “FINRA is losing money and members because they’re going to the RIA fee-only model. If FINRA gets its way, [it] will do everything in its power to require everyone to be affiliated with a BD firm and regulate the small RIAs out of the business, just the way they’ve regulated the small BDs out of business.”

Other advisors take issue with Fisher’s contention that the Securities and Exchange Commission “hasn’t thought through the implications” of FINRA’s bid to regulate RIAs.

As Evensky notes, the commission’s hands simply may be tied. “I disagree that the SEC doesn’t have a clue. The SEC understands the issues very well. The problem the SEC has is politics. I don’t think they can do what they perhaps want to do. My concern is that they might not be able to do anything and then the [fiduciary-standard matter] becomes a moot point, kind of frozen. Lobbying is trying to prevent the Department of Labor from taking action.

“There’s a good chance the SEC may never do anything,” Evensky says. “Or if they do, it will be a new universal fiduciary standard — they’ll use the word fiduciary, but it will have no relationship to what the concept of fiduciary has meant for hundreds of years.”

Carson is clearly in favor of all advisors being held to a fiduciary standard. “The marketplace believes that we’re all operating under it, but that is not the case. So if the marketplace believes that, don’t we owe it as an industry to give them what they think we already have?”

The ultimate solution, Evensky conjectures, may be for “investors to give up on Congress and regulators, and protect themselves.” Indeed, this advisor has already started down that path. Evensky’s firm has what he terms a “mom-and-pop commitment,” signed by clients, that doesn’t even mention the word, fiduciary. It states that the client’s interests will be placed first and that conflicts will be eliminated.

“Investors,” Evensky says, “are going to have to look out for themselves.”